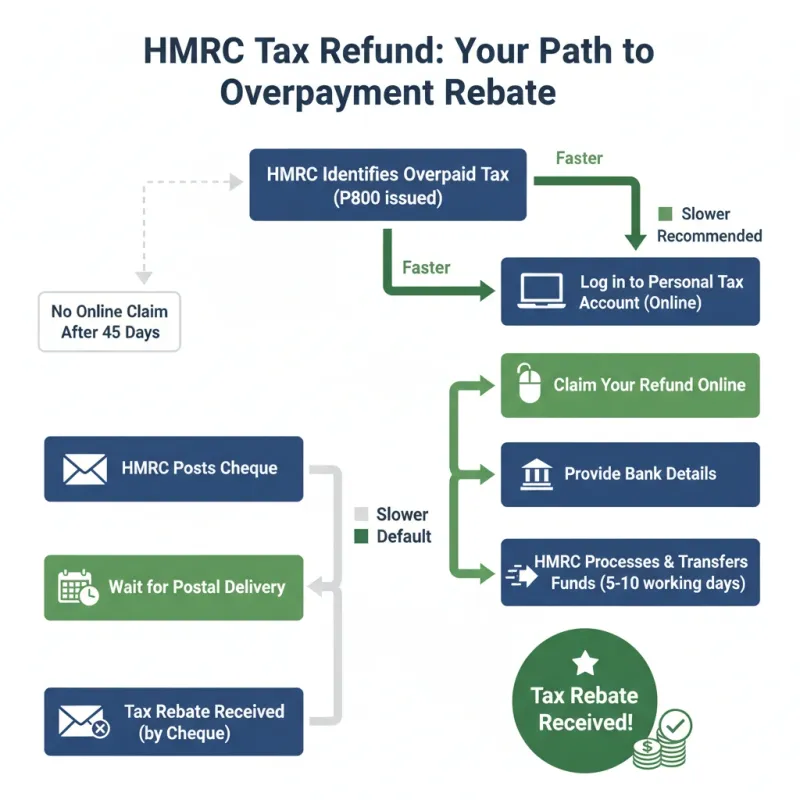

The Unclaimed Tax Surplus: Why UK Businesses Are Leaving Their Own Money in HMRC's Accounts

Photo: HMRC tax refund business accounting UK finance documents, via taxcalculatorsuk.co.uk

The Unclaimed Tax Surplus: Why UK Businesses Are Leaving Their Own Money in HMRC's Accounts

The relationship between UK businesses and HMRC is most commonly understood in one direction: the authority demands, the taxpayer pays. What receives far less attention is the reverse flow — the substantial volume of tax that businesses have paid in excess of their genuine liability, which sits within HMRC's systems awaiting claims that, in many cases, never arrive. This is not a marginal phenomenon. Independent estimates suggest that billions of pounds in legitimate tax repayments go unclaimed by UK SMEs and limited companies each year, not through any deliberate choice, but through a combination of incomplete advice, administrative oversight, and simple unawareness.

For business owners already managing the demands of day-to-day operations, the notion that they may have overpaid tax can seem abstract. The following analysis makes it concrete.

Corporation Tax: Where Overpayment Begins

Corporation tax self-assessment places the burden of accurate calculation squarely on the business. HMRC does not proactively identify when a company has paid more than it owes — that responsibility belongs to the taxpayer. In practice, this means that errors made at the point of submission tend to persist unless the business or its advisers actively review historical filings.

The most common source of corporation tax overpayment is the understatement of allowable deductions. Businesses regularly fail to claim the full range of expenses to which they are entitled, either because their advisers are not sufficiently familiar with their operations or because the relevant expenditure was not identified as tax-deductible at the time it was incurred. Capital expenditure misclassified as non-qualifying, professional fees incorrectly treated as non-deductible, and losses from earlier periods not carried forward or back appropriately — each of these errors, individually modest, can accumulate into a meaningful overpayment across multiple accounting periods.

The time limit for amending a corporation tax return is generally two years from the end of the relevant accounting period. Beyond that, claims must be pursued through a formal overpayment relief application, which carries a four-year limitation period from the end of the relevant tax year. Business owners who have not reviewed their corporation tax position for several years may find that some overpayments are already beyond recovery — but many will not be, and the urgency of acting before further windows close is real.

Capital Allowances: The Persistently Underutilised Relief

Capital allowances represent one of the most consistently underutilised areas of UK business taxation. The Annual Investment Allowance, the structures and buildings allowance, and the various special rate pool provisions together offer substantial relief on qualifying capital expenditure — but only if the business identifies and claims them correctly.

The embedded capital allowances issue is particularly significant for businesses that have purchased or refurbished commercial property. A proportion of the purchase price or construction cost of most commercial buildings is attributable to qualifying plant and machinery — electrical systems, heating infrastructure, security installations, and similar items — that attracts capital allowances at rates far more favourable than the structure itself. Historically, many businesses and their advisers have failed to undertake the detailed surveys necessary to identify and value these embedded items, resulting in systematic underclaiming that can persist across the entire ownership period.

For businesses that have acquired commercial property in the past four years without a specialist capital allowances review, the potential for retrospective claims is considerable. The exercise requires a qualified surveyor working alongside a tax adviser, but the returns frequently justify the investment many times over.

Research and Development Credits: A Relief Claimed by Too Few

The UK's R&D tax credit regime was designed to incentivise innovation across a broad range of industries, and the definition of qualifying activity is deliberately wide. Nevertheless, the proportion of eligible businesses that successfully claim remains disappointingly low. Many SMEs operate under the misconception that R&D relief applies only to dedicated research laboratories or technology companies, when in fact qualifying activity can arise in manufacturing, food production, construction, engineering, software development, and numerous other sectors.

Qualifying R&D does not require the development of something entirely novel to the world — it requires an advance in science or technology, or an attempt to achieve one, that involves the resolution of genuine technical uncertainty. A manufacturer developing a new production process, a construction firm engineering a novel structural solution, or a food business reformulating a product to meet new regulatory standards may each be undertaking qualifying activity without recognising it as such.

The financial consequences of missing R&D claims are significant. Under the SME scheme, qualifying companies can claim an enhanced deduction of 186% on qualifying expenditure (at current rates, following recent reforms), with loss-making companies able to surrender the credit for a cash payment from HMRC. Claims can be made retrospectively for up to two accounting periods, meaning that businesses which have never claimed — or which claimed incorrectly — may have a meaningful sum available if they act promptly.

CIS Deductions: A Specific and Frequently Overlooked Refund Route

For businesses operating within the construction industry, the Construction Industry Scheme creates a specific and frequently mismanaged tax position. Subcontractors who have not obtained gross payment status have tax deducted at source by contractors at either the standard rate of 20% or the higher rate of 30%. These deductions are credited against the subcontractor's corporation tax or income tax liability, but the mechanics of the offset process mean that overpayments are common, particularly for businesses whose annual tax liability is lower than the cumulative deductions suffered.

Many subcontracting businesses fail to reconcile their CIS deductions against their tax liability with sufficient precision, either because their bookkeeping does not capture deductions systematically or because their year-end process does not adequately address the offset. The result is an overpayment that sits within HMRC's systems, recoverable through a formal repayment claim but only if the business identifies the discrepancy and pursues it within the applicable time limits.

VAT Overpayments: The Error Correction Framework

VAT overpayments arise through a variety of mechanisms: incorrect output tax applied to exempt or zero-rated supplies, input tax recovery missed on qualifying expenditure, and errors in partial exemption calculations among them. HMRC's error correction framework permits businesses to adjust historical VAT errors on a current return, subject to a four-year time limit and monetary thresholds above which formal disclosure is required.

Partial exemption is a particularly fertile area for overpayment. Businesses that make both taxable and exempt supplies are required to apportion their input tax recovery, and the standard method prescribed by HMRC does not always produce the most favourable result. The special methods framework allows businesses to adopt an alternative apportionment approach that more accurately reflects the use of inputs — and for many businesses, the adoption of a special method, applied retrospectively where applicable, generates a meaningful repayment.

The Action Imperative: Why Delay Is Costly

The common thread running through each of these overpayment categories is the existence of a claim window that is actively closing. The four-year limitation period that governs most retrospective tax claims means that overpayments from accounting periods ending in 2021 will, in many cases, become permanently unrecoverable during the course of 2025. For businesses that have not reviewed their historical filings in recent years, the urgency of acting now — rather than deferring to a more convenient moment — cannot be overstated.

The practical starting point is a structured review of historical tax returns, ideally conducted by an adviser with specific expertise in the relevant relief areas rather than a generalist. Where the initial review identifies potential overpayments, a more detailed analysis can quantify the claim and assess its prospects before any application is made.

The money is there. The question is whether UK business owners will act in time to recover it.